As a multifamily investor, title insurance is something you really need to have. It protects you from existing problems when buying real estate. You must start protecting the equity in the properties you are investing money into.

Join Ava Benesocky and August Biniaz as they talk to the Managing Director of MBL Title, Lee Small. Learn all you must know about title insurance, from why you need it, how to do it, to how to handle the challenges along the way. If you are eyeing a property for purchase, this conversation will certainly be a huge help to keep yourself protected.

Get in touch with Lee Small:

LinkedIn: https://www.linkedin.com/in/lee-small-40b346a6/

Website: https://mbl-title.com/

If you are interested in learning more about passively investing in multifamily and Build-to-Rent properties, click here to schedule a call with the CPI Capital Team or contact us at info@cpicapital.ca. If you like to Co-Syndicate and close on larger deal as a General Partner click here. You can read more about CPI Capital at https://www.cpicapital.ca. #avabenesocky #augustbiniaz #cpicapital

—

Watch the episode here

Listen to the podcast here

Important Links

- MBL Title

- The World of Golf

- Phil: The Rip-Roaring (and Unauthorized!) Biography of Golf’s Most Colorful Superstar

- Lee Small

About Lee Small

Lee Small runs national business development for MBL title, a title and escrow company based in Dallas, Texas. Lee discusses transactions and industry trends with clients in all commercial asset classes and helps close complex transactions. Lee received his MBA from Pepperdine University and has closed over $1.5B in transaction volume during his career.

Lee Small runs national business development for MBL title, a title and escrow company based in Dallas, Texas. Lee discusses transactions and industry trends with clients in all commercial asset classes and helps close complex transactions. Lee received his MBA from Pepperdine University and has closed over $1.5B in transaction volume during his career.

Why Multifamily Investors Need Title Insurance With Lee Small

We are joined by Lee Small. We are excited to have him on here. We met Lee in Vancouver. We went out for dinner with him for the first time. What an amazing guy. What a funny guy. I laughed a lot at that dinner.

When I hear Lee Small, I remember my favorite rapper, Biggie Smalls.

I’m also a New Yorker, so we are good.

No connection there. For all the kids reading this, thinking about what you want when you grow up, you want to be what Lee is doing, going out for lovely lunches and dinners, much so that he doesn’t even have a chance to go out with his own wife. He gets taken out so much for lunches and dinners at his company’s expense is one of the greatest jobs out there. We will get into all of that.

It’s a pretty cool job.

We feel like it’s an important topic to cover as well. It’s about title insurance. I will get into this briefly here. Obviously, we are located here in Canada. We invest in the US. We partner with Canadians and Americans to buy US real estate but a lot of people reading this are Canadians who are involved in Canadian real estate.

We don’t have title insurance here in Canada. The process is that when a title has been transferred here in Canada when a property is sold, and there is a change of ownership in a property when that change takes place, nothing can linger on. If there was a builder’s leaned, if there was some type of mortgage, if there was anything on the property, after that transfer takes place, nothing goes on.

I will get into this a little bit later on but even in cases of fraud, nothing can take place because a title has not been switched. In the US, that’s not the case because of the potential for litigation or other issues or something on the title that will linger around to the new owner. That’s why you got to get title insurance. It’s always important to get insurance. Another important thing about title insurance is that usually you get insurance for something that might happen in the future but title insurance is from anything from the past where we will get Lee to get into it. Maybe you can tell our readers a little bit about Lee.

Let me do a quick introduction about Lee and his background. One thing I want to mention is that there’s not a lot of content online about title insurance. We are excited to bring a lot of value to people. A little bit about our guest, Lee runs national business development for MBL Title, a title and escrow company based in Dallas, Texas. Lee discusses transactions and industry trends with clients in all commercial asset classes and helps close complex transactions. Lee received his MBA from Pepperdine University and has closed over $1.5 billion in transaction volume during his career. Welcome, our good friend, Lee.

Thank you so much for having me, guys. It’s great to see you.

It’s great to see you, too. We can’t wait to dive into things. Can you start by talking to us about your background and then your start in real estate, please?

My experience is a little bit different than a lot of people who hopped into real estate. At least a lot of people do here in Texas. I was a sports television anchor for two local TV stations in the State of Texas for five years after graduating undergrad. I covered a lot of college football, college baseball, college basketball, professional football, the Dallas Cowboys, and the Texas Rangers baseball team. I had a great time covering sports for five years. That’s all I wanted to do when I was growing up. Through a couple of connections, I ended up getting into oil and gas for a short time in West Texas. The oil market, unfortunately, crashed in 2014. That was a career reset for me.

I went back to school at Pepperdine and got my MBA and moved to Dallas, and got into national commercial title insurance. Here we are, still a national title. The landscape here for the commercial real estate stuff and across the Southeast has changed rapidly over that time. I’m excited to be here and talk to you guys about title insurance and why it’s important in the whole process.

What is title insurance? Why is it needed? You shared a great story with us at the dinner that we shared that we had in Vancouver. Maybe you can tell.

The story that where title insurance even came from. What was the impetus for title insurance?

There are a couple of interesting things about title. The title is one of the rare forms of insurance that was not already over in Europe before America was founded. It was created here in the United States. It’s also the only form of insurance that covers what has already happened. It takes a second to wrap your head around that because it’s such a foreign concept of insurance.

Title insurance is the only form of insurance that covers what has already happened. Share on XCar insurance or health insurance are all forward-looking things. Title insurance in the United States covers what has already happened. You are saying to yourself, “Why would I need insurance for something that has already happened?” Here’s where title insurance comes from. In the late 1800s in Pennsylvania, there was a transaction between two parties.

I will get into more detail about what that means here but I will shorten the story to give the history of title. During the search and exam process of what public records were out for this property, it came to be founded that there was a lien on the property being sold. The attorney went to get an opinion on that lien of whether or not it was valid.

The opinion came back. They said, “This lien is not valid. You can proceed with this transaction. It will not affect the buyer of this property.” It turns out that was incorrect, in fact. This new buyer purchased this property, paid full price, and then it was foreclosed on by the county and the sheriff to recoup that lien because that is the collateral for that lien for taxes. They sold it. There was nothing left of his property. He had paid full price. They had taken it from him to sell it for this lien that was valid.

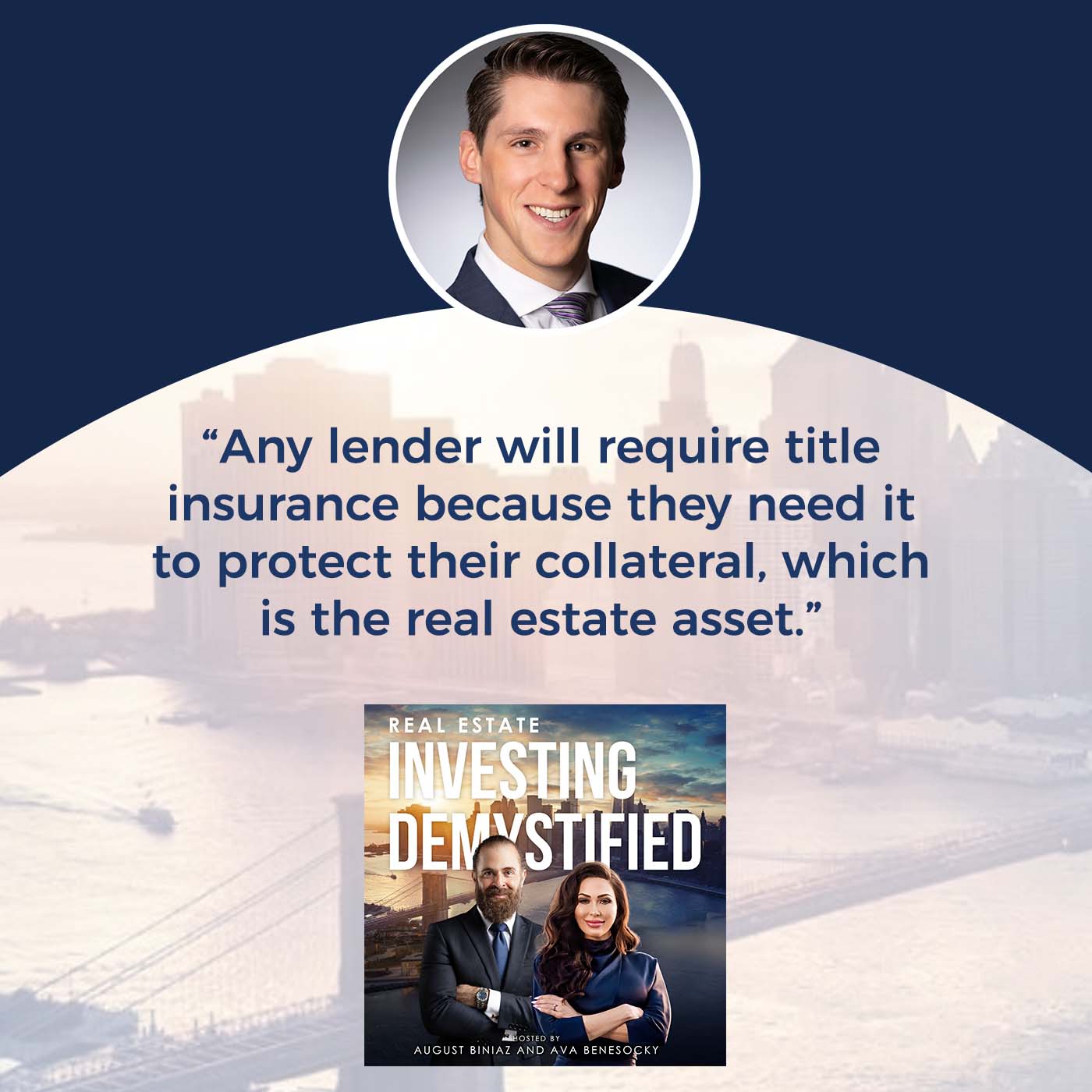

As it went through the courts, they realized that the parties hadn’t done anything wrong but that there needs to be a form of insurance for situations like this that move forward. It’s not just commercial, to be clear. This title insurance is important for single-family. For any lender in the United States, for the most part, this is a broad generalization but any lender will require title insurance because they need it to protect their collateral, which is the real estate asset.

That’s how we got to have title insurance in the United States. It has grown. There are multiple different underwriters like you have for life insurance and all these other groups that are some big underwriters who will underwrite the actual title insurance. We are involved on the national commercial side in any commercial transaction, multifamily, hospitals, industrial, cold storage, self-storage, manufactured housing, and anything that transacts. We also have a whole single-family division, which I don’t work directly on. We are involved in any transactional process for real estate in the country.

Title insurance is like a history lesson on that piece.

For me to add one quick thing here, in Canada, we are still archaic but what happens is that if a situation like the story you shared takes place here in Canada, the lawyers’ errors and emissions come into effect. Also, we have an actual government institution, which is the land title that does the transfer. You got the lawyer or notary public that does the transfer. I’m sure you’ve dealt with them many times. That’s how we mitigate issues with title transfer.

The next question I was going to ask you, and you touched on it. You said lenders need title insurance to protect their collateral. That was our question. Is title insurance a requirement if there is debt financing involved or by different levels of government, county, state or federal?

The short answer is yes. Again, there are some rare exceptions where that’s not exactly the case. There are two forms of title insurance. It’s important that it’s not just the lenders who are wanting it and desire title insurance. There’s what we call an owner’s policy, which covers the ownership. For my house exactly, I have the owner’s policy. There’s a lender’s policy, which covers the lenders.

Title Insurance: There are two forms of title insurance. The owner’s policy covers the ownership of your house and the lender’s policy covers the lenders.

For example, if you are refinancing a multifamily property and the ownership group is not changing, you only need to purchase a new lender’s policy because the ownership group is not changed. If you were transacting and you are selling the property, and the new buyer is going to both change, obviously a different ownership group, and then a lender is going to come on, you will get both policies.

However, in the State of Texas, and there are some others across the country, when you package them up, the cost comes down quite a bit on the lender’s policy. In Texas, if you do it simultaneously here, you pay for the owner’s policy, and then you will pay $100 to add on the lender’s policy, which is cheap. That’s because you are packaging them up at the same time.

If you are doing a refinance, that doesn’t come into place. We have some other refinance R-8 credits that come into play, which are too granular for this. If you have real questions, people could reach out to me about specific refinance stuff and how the pricing works because each state is different in the United States. You do typically during a sale or purchase package those two up together.

I wanted to quickly elaborate on the cost of title insurance and what’s the price. It is the assessment by the county but is it also the recently sold price? How do you figure out the title insurance price?

The title is calculated by the purchase price or the refinance price. It’s not by the appraised value. That doesn’t go into effect at all. If you put a property under contract and it’s $10 million, the amount of title insurance assuming you get coverage for the whole part in the owner’s policy, you are getting a $10 million policy. That would cover the entire portion because that’s what the purchase price is.

Title insurance is calculated by the purchase price or the refinance price instead of the appraised value. Share on XYou have to remember the reason you get that full coverage is that in the instance where you have a total loss of your investment if something comes back where it turns out the person you bought it from didn’t own it and didn’t have the right to sell it to you, while the person who did rightfully own it has to get their property back or has to be paid to settle, in which case the property has been valued and the fair market at $10 million.

That’s the amount that you could potentially lose if you had purchased something from somebody who didn’t go through the process and no one caught that there had been an issue. It would be a $10 million claim against the title insurance company. It comes down to either the purchase price you pay, how much you are ever developing it for or the refinance amount from the lender.

When you have the seller’s and the buyer’s policy, usually in transactions in a competitive market, do the seller and the buyer pays for their own policy? We know that in real estate transactions, for example, the seller is who pays for both buyer’s and the seller’s agent but what happens in a policy situation?

It depends on the state. In Texas, for example, it’s customary for the seller to pay for the owner’s policy. The purchaser will pay for any endorsements, which are added on coverage that their lender is usually requiring. They will pay for the loan amount as well. It gets split out but most of the cost is shifted to the seller. There are many instances we still see where because of the competitive market, the buyer is pushing hard and wants to use their title company.

Sometimes they will pay the title premium because they want to use the person that they know and trust. In other states also, it is very much up in the air on who pays for the title insurance. It goes back and forth, and all these things while they are negotiation points during the transaction. Each state has a cultural norm for who traditionally pays. I wish there were a more cut-and-dry answer but it’s not as easy as this is exactly who pays what every single time because it does change.

If the prices don’t change, for example, in your state, the price is set in stone, and every provider has to go by the same ratio or the same price, how do you compete? A business like yours, how does it work? Is it mainly sales and marketing? How do you compete in a business where the price is flat across the board?

Most states in the country are not set-rate states. Texas happens to be one of them. The rates are set by the Texas Department of Insurance. In Texas, we are winning business for a couple of reasons. The way how we win business is twofold. Getting back to the underwriters that I mentioned previously, we have more underwriting options to go to solve problems.

Oftentimes, every deal has some complexities with it. Most things are not cut and dry, clean and easy every single time. Having a number of different underwriters allows us to go to those underwriters. People forget. They think of it sometimes as a commodity because the price is set. They assume everyone is going to look at it the exact same, and their policy is going to come back the exact same.

This is insurance, after all. We are talking about a determination of risk by these underwriters. We work with our underwriting partners on determining what risk level they are willing to take. Some of them are willing to absorb more risk and make it a smoother transaction without going through all these hurdles that maybe another underwriter will.

From that sense of having more underwriters to go to, that’s one way, we win business. The second way is we have who we think are some of the best attorneys and commercial closing attorneys in the entire country. Our people are extremely sophisticated and good at working with buyers, sellers, all the council members, and everyone involved in the transaction. They are extremely sophisticated people.

That’s not the case. You don’t have to be an attorney to close deals but we feel like it makes for a better closing experience because they are more sophisticated. That’s where we add value to the transaction and make things easier for our clients. It’s important to mention that because Texas is set, most other states are what are called file rate states. Roughly 40 of the 50 are file rate states. What that means is that every year, each insurer underwriter will file their minimum rate.

Title Insurance: In file rate states, each insurance underwriter will file their minimum rate every year.

They say, “For every $1,000 in coverage, this is how much it’s going to cost for title insurance.” That’s the bare minimum.” You can charge more than that but there is a fluctuation in price. In some states, if you go to some of our underwriting partners, First American Fidelity, and Old Republic Stewart, if you go to each of those, your price will vary. Some people in those instances could pay more or pay less but there is a set for what you have to charge title insurance in those file rate states.

Going back to Texas again, the price is par price across the board but the service is different. The onus is on you. If you make a mistake and there is something on the title that the buyer or the seller is off the hook for, you have to recoup that. That’s why people are buying insurance. You are saying that it’s more about the process, the underwriting. It could be done quickly when the transaction takes place in a lawyer’s communications. Is that what you were talking about?

Taking aside after the policy is issued and if there were any claims issues, that stuff is a set process that happens at a specific point in time if there is an actual title claim on the insurance policy. This will make it a lot easier. I will walk through the entire process real quickl. You guys put a multifamily property under contract. At this point, we will receive the contract. We will go back through all public records on this property, on this tract of land, and pull everything that’s a public record. It could be liens or anything that affects easements. You have water lines, you have electricity lines, it could be anything that affects it. We will put together what is called the title commitment.

The title commitment then goes out to all the parties. It lists three sections. You have schedule A, which is your property description, plan lines, and everything that is the formal description of the piece of property you are subject to purchase. Schedule B is your exceptions, which list out things that we are not covering, we are accepting.

For example, if you put a property under contract and it is of public record, that they could run a power line straight over the top of your building. If the state electricity board comes and decides to run that electricity pole right over your building, we are not covering it because you knew about it before you purchased the property that was of public record. That is a schedule B item that is listed in the public record. We are making it known to both parties that it’s out there.

You must mention it even though it’s a public record in your report.

Our purpose is that we are not coming up with these facts out of thin air. The only job for us is to discover what is a public record, do some research on the property, and present that information so that both buyer and seller have an understanding of the property that they are supposed to be transacting on. One of our key roles is determining what’s out there and making sure people are aware of that. Schedule B is an important section. Both sections are important for different reasons. You get to schedule C, which are items that must be taken care of for us to issue the title policy as laid out in the title commitment. You always have to prorate taxes. You have to take care of the Tax Bill.

You might need to show entity docs. There are all of these things that you’ve probably seen throughout the process of buying and selling properties where you have to show certain things to make sure, again, that you have the legal authority to do it, that you have all the signatures, all of these things that go into making sure that we have all the information we need to produce that title policy. That’s the process. Once you close, you fund your money into us. We will distribute it to the parties, the sellers, and all the people as it’s laid out in the contract.

That’s only if you are representing us on the escrow side. Is that right or no?

The US is different in that. Each state does a little bit differently. If you go to California, title escrows are split into two separate entities. In Texas, our title and escrow, the same person that is handling the title is the same group is also handling your escrow is also handling both that. We think it’s easier because it’s the same office. It’s the same group of people. It’s a cohesive unit that’s handling both your title stuff and your settlement statement and disbursement of funds. That makes it a little bit easier because you don’t have another party involved that’s a bunch of other people.

That’s regulation. That’s not a choice you guys have made.

You probably could be a standalone escrow office, and some people do for M&A transactions Oftentimes, in the title and escrow space, everyone in the State of Texas is set up to both do title and escrow because it makes it much easier for people. We will distribute the funds. I forget the exact amount of time. It’s 30 days, maybe 60 days, to produce the actual policy. You still have the policy. It has to be produced, sent to you, signed, and everything like that. The coverage begins as soon as you close. That policy is sent to you, and you should keep it on file.

If anything happens where there is a question regarding ownership in the property, anything that comes up, if someone comes to you and says, “You guys developed on the corner of my land. You need to pay me for it because that was my land, that little acre or that little parcel over there,” then you come to title. That’s where we get involved. We have somebody again who comes back and says, “My husband sold you that property but I didn’t sign and we weren’t officially divorced at the time of signing it. I never signed any documents.” That’s going to be a big title issue.

Those are small issues. It could be survey issues. Oftentimes, we joke about how much fun I get to have on my job with meeting a whole bunch of people and going out for a lot of lunches and dinners, and I could write a great review about restaurants around the country. The importance of title, I can’t stress this enough, is locking in your value and your equity in the property that you are putting money into. You can go in with certainty that if something happens, you have that title policy that will protect you and the amount of money you’ve put into that property to purchase it. That’s an important thing.

It’s one of the reasons that real estate has been resilient over the years is that we have an instrument that allows us to ensure the value of what you’ve paid for it, at least on the ownership side. It doesn’t mean the market won’t go down and that people might not pay the same that you paid for it because the market swings but the amount you put into it can never be taken away because of an issue with an ownership issue from a title perspective. That’s an important thing that people should pay attention to, and want someone quality on the title side helping them out.

Talking about all the issues that you brought up, do you have any data on as far as the issues that come up on what is the rate that the insurance that you sell? I’m sure car insurance companies and life insurance companies all have these stats that 98% of the time, the person is not going to die by the age that we are guessing that they are going to pass away. With you guys, do you have any data on how many of the insurances you sell on title come back with some form of delinquency or litigation or some form of caveat that you now have to deal with? Do you have any stats on that or stories you can share?

It’s a little loose, probably, but I’ve heard that 4% is the claim percentage across the entire country for title insurance. If you look at that compared to auto or home, it’s a lot lower. What I will say is you have to remember we are talking oftentimes, especially on the commercial side, we could be talking about a $250 million building.

I didn’t thankfully have this but I’ve heard of people who have developed buildings, and the surveyor again messed up one of the corners. They ended up developing a large building, and it was 1 square foot that they had gone over the property line. They had to take that 1 square foot, the value all the way up the building, and pay off the person whose property it is.

The survey comes in a way after.

The survey comes in before. The survey process comes in if it’s already established.

Do you guys require a survey to take place when a transfer is taking place prior to the transfer?

The survey is not fully required but oftentimes, the lender will want survey coverage. If you want to add the survey coverage as an endorsement, you obviously have to provide a survey.

We don’t have that here.

When it’s land, that’s a much different story than what you are most of the time dealing with. There will be a survey most of the time. Sometimes it has to be updated. This is interesting. It could be a 40-year-old survey but if it still is as built and represents the dimensions as they are in the current day, we can use that survey as long as it meets certain specifications. If it doesn’t, if a little shack has been built on, and there are other buildings that have been added, we are going to need a new survey because the dynamics of that asset have changed.

We syndicate deals. We put a property under contract. What happens in a case where the earnest money goes hard on day one? When do we get the title insurance involved?

There’s no hard and fast rule. I always tell people that the sooner, the better. It depends on where you are interacting and where you are transacting in. In Texas, for example, our cost of pulling all that title commitment and getting that all together is free. You pay for it when it closes. If you are working under good faith, expecting something to close, and we start pulling the title commitment as you guys are drafting the contract and it gives you an idea of what is out there, it very well could come back and have an issue on there that you no longer want to proceed with that property. We hope that doesn’t happen but it is an information tool that you can use as you are working through putting that building under contract.

When a property is put under contract, the sooner you get title insurance involved, the better. Share on XSome people wait until it’s under contract. That comes to us. We pull the title commitment is usually 3 to 5 business days, turn it around, and send it out to all the parties. It also depends on which county and state you are doing work in terms of timelines. Sometimes the more rural you get, the longer it takes for title commitments because you have a smaller pool of people in those counties that are in what is called title plants.

This is a weird term but they are called title plants because back in the day, they used to have all of the recorded paper, and there was so much paper, they called it a title plant because they come from trees. It’s called a title plant. They have those all over the country in different counties. Some of them are privately owned. Some of them are publicly owned. Again, probably too much detail but it’s a fascinating look behind the curtain at how things are done here. It’s a little different but it also is extremely important.

Talking about the journey again for an investor or a group looking to bring on tens or hundreds of investors, obviously, we have a fiduciary duty as general partners. If anybody is going to invest with us in the future, the last thing you want is that you won’t have any issues through any part of the process. A group or an investor, when should they engage their title insurance advisor when it comes to that process where in a competitive market, a lot of times there’s a deposit put, and the deposit goes hard day one? Is it safe to say that as soon as the deal comes across your desk and you send out the LOI, engage the title insurance specialist?

It goes back also to the attorney you are working with and how they draft the contract because oftentimes, we will see that even if there is hard money on day one, there is a stipulation in there that this money is hard unless there are title issues. That’s a broad, vague term. There are title issues. It just depends on the severity of them. We do see that sometimes but that could go to litigation because the other side might say, “That’s not a real title issue. We are keeping your funds.”

Like you, guys, we are fiduciaries. We don’t act on anyone’s behalf. We are simply there to interpret the contract that has been written and produce these documents that are of public record for both sides. We don’t have a dog in the fight. We are just interpreting a contract. The earlier you are working on something and putting it under LOI, it’s always a good idea to have a partner that’s starting to work on that for you.

Title Insurance: As an investor, engage with your title insurance advisor early, even before writing an LOI. It’s always a good idea to have a partner working on that for you.

Last question here before we move to the next segment of our show. It’s not really a question. It’s more of a comment. I want to blow everybody’s mind. I did a little bit of reading about this. Here in Canada, when a property is transferred, the moment that transfer takes place, if there was some kind of fraud taking place, the property belonged to John Smith but somebody stole their identity. That transfer was taking place. The new owner now has positioned. Even if it was proven there was some form of fraud, the new owner keeps the property.

Even if the new owner knew there might have been fraud taking place, as long as the new owner was not involved in the fraud and was not benefiting and being part of the fraud, even if they knew there was something fishy happening here, they still get to keep the title. We had to put that information out there. The next segment of our show is the fun and exciting stuff. If it wasn’t exciting enough for you, guys, have some fun now.

Here we go. The 10 Championship Rounds to Financial Freedom. Number one question, who was the most influential person in your life?

My parents, for sure, when growing up. Both my parents were doctors and well-educated, smart, and driven. They gave me every opportunity I needed in life to be successful. Without them, I wouldn’t be where I’m at now.

I was going to say that Apple fell far from the tree in this situation but he married a doctor. He made up for it.

Lee, what is the number one book you would recommend?

Top of mind, I’m a big golf fan, and there’s a lot if you have been following The World of Golf as someone in turmoil. I would highly recommend it if you are interested in everything that’s going on. Also, a great autobiography from Alan Shipnuck about Phil Mickelson. It delves into the Saudi stuff that’s going on. It also has a lot of information on Phil’s legacy in golf. Good book, especially if you are a golf fan.

Phil: The Rip-Roaring (And Unauthorized!) Biography Of Golf’s Most Colorful Superstar By Alan Shipnuck

You said all the Saudi stuff that’s happening. There’s a Saudi connection to golf?

Yeah. We can do a whole other episode. We can get into that at a later time.

If you had the opportunity to travel back in time, what advice would you give your younger self?

I would say enjoy the moment. One of the funny things is that we get older and we get a little bit more established to maybe make a little bit more money. We still have those memories of the times when we were dirt poor hanging out with our college buddies or buddies somewhere. Those are some of the best memories you have ever made. You wish you would go back and enjoy them more.

Life is not about the money, and it’s certainly not about getting somewhere. It’s about the journey of getting there. Enjoying that journey. Even though there are difficult things along the way that make it uncomfortable, that’s what makes life enjoyable, and it’s the people you are doing it with. I’ve tried to focus on that. I would tell my younger self to focus on the journey.

Difficult things make life uncomfortable. But that's what makes it truly enjoyable and the people you're doing it with. Share on XWhat’s the best investment you’ve ever made?

Real estate. It has been a good market so far. We will see how things are rapidly changing here. The real estate investments I’ve made both in multifamily and industrial have done well. I love the real estate sector.

What’s the worst investment you’ve ever made? What lesson has been learned from it?

Single stock picking. I’m horrible. I don’t even have that many individual stocks but I have a good knack for buying at the top and waiting to sell at the bottom. Single stocks are not my bag of tea.

How much would you need in the bank to retire now? What’s your number?

I would probably say $5 million, and I would be good. As long as I can play some golf and hang out, both healthy and you can travel. You don’t need too much. Some people need $100 million. You can give me $5 million, and I’m good.

If you could have dinner with someone, dead or alive, who would it be?

Any of our early Presidents, George Washington and Abraham Lincoln. Their perspective also on what they went through and the difficulties that are going on in politics these days, you would realize that politics has always been difficult. Their stories from the war and Civil War and all that stuff would be fascinating to listen to.

Getting assassinated over their beliefs.

If you weren’t doing what you are doing now, what would you be doing now?

Honestly, I never thought I would be anything other than a TV sports anchor. I saw my parents as doctors. I never wanted to go down that path, even though I married a doctor. It didn’t fall too far from the tree but I would be back doing sports journalism again.

Book smarts or street smarts?

Street smarts. Not even close. Don’t put a test in front of me. I’m fine. I’m going to get by. I’m going to pass. I need more street smarts.

Last question, if you had $1 million cash and you had to make one investment now, what would it be?

The real estate’s what I know. It’s what I trust. I’m smart enough to know I’m not the GP in a GP role but I know a lot of smart people who are GPs. I would be happy to find some good investments and hang on for the ride in real estate. The stock market would be all the other stuff I don’t understand and like as much. As Warren Buffett always says, “Invest in what you know.” For me, it’s real estate. I will stick to that.

You are in the know because you are right there in the trenches with all the GPs and investors. People should come to you when they want investment advice when it comes to real estate. We appreciate it. Thank you for being with us here.

Lee, what’s the best way people can reach you?

LinkedIn is great. You can find me on LinkedIn. MBL-Title.com, you can see our company and my bio, and all that stuff is up there. If you have any questions, please feel free to send them my way. I’m always happy to help.

Lee, it was incredible seeing you again.

It’s great to see you guys again. Hopefully, I will be across the border sooner than later. Let me know if you come to this side as well. We will have to get together again.

We are coming your way.