Over the last week or so, there has been a significant amount of debate in the media about “yield curve inversion” in the bond markets and what this may mean for the US economy and, perhaps more importantly, for real estate markets across the country.

Buy what is yield curve inversion and why does it concern stock, bond and real estate investors so much?

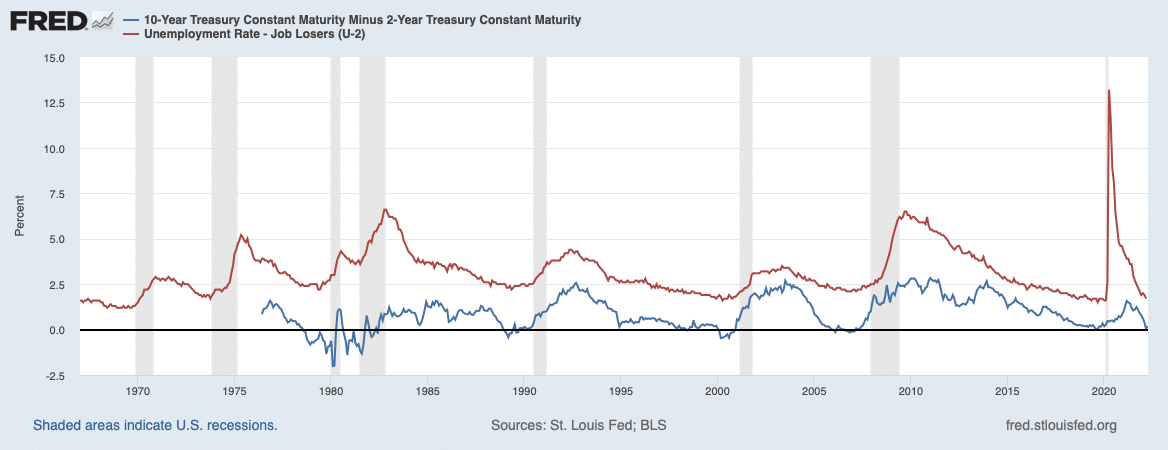

Yield curve inversion

Fundamentally, this is a phenomenon which occurs in the bond market when the yield curve on the Treasury 2-year bonds exceeds that of 10-year bonds.

The yield curve applies to US Treasuries of various durations and typically shows longer-dated Treasuries, such as those with 10-year or 30-year maturities, as having higher yields than shorter-dated Treasuries such as 3-month or 2-year maturities.

However, it’s the 2-year and 10-year bonds which are watched more closely because they are amongst the most commonly traded. An inversion in these particular bond rates has correctly predicted a recession with a lead time of between eight months and two years in each of the last eight recessions.

Certain points of the yield curve have already inverted in recent weeks (the 3-year and the 5-year on March 18th, the 5-year and the 30-year on March 28th).

Although other live measures showed inversions briefly occurring intraday on March 29th and again on March 31st, the U.S. Treasury did not initially recognise such inversions.

What is the significance of yield curve inversion?

An inverted yield curve is important as it is often seen as a signal that investors are less confident about the short-term economic outlook than the longer term, forcing interest rates on short-term bonds to move higher than those paid on long-term bonds.

To many investors this is an early warning sign that the US may be facing a recession in the coming 12 months or so, as these inversions have preceded most every recession over the past 60 years (bar the 1998 recession).

Before we go further, let’s just take a moment to review what an “economic recession” is as the phrase itself has seriously negative connotations. However, it is important to note that it may not always involve a deep or protracted economic downturn, and one which may or may not be country wide:

A recession can be defined as: a decline in economic activity across an economy, lasting more than a few months, and evidenced

by a fall in real GDP, real income, employment numbers, industrial production and retail and wholesale sales.

So, such yield inversion doesn’t mean that the value of stocks will suddenly drop, real estate prices fall and unemployment increases. The inversion may indicate that a recession or a period of reduced economic growth and increased unemployment is likely but this can sometimes take years to take effect.

For example, the yield curve inverted in 2005, but a recession didn’t start until 2007. The most recent inversion in September 2019 prompted fears of a recession but this didn’t materialise until 2020 and was then, mainly, due to the effects of the pandemic.

Whilst yield curve inversion by itself does not indicate a recession, the likelihood of falling into a recession could be enhanced by other factors and sentiment which created the conditions for the inversion—one key factor being the current administration’s economic policies which have driven the budget deficit to new highs.

Having said all of this, given the Federal Reserve’s unprecedented attempts to control inflation, with a recent interest rate increase being just the first of many planned increments over the next 12-18 months, many experts maintain this recent yield curve inversion may be different from those in the past in view of the relatively robust health of the US economy.

Economic indicators for real estate investors

Any professional real estate investor will constantly monitor key economic indicators to gauge the health of the domestic economy nationally, and especially the health of local real estate markets into which they invest. As we’ve said before, real estate markets across the US are not homogenous and some will move upwards whilst others stagnate.

There are several core economic indicators are closely watched to assess the outlook for the real estate sector and, by extension, real estate investors, namely:

- Consumer spending—current and outlook;

- Employment rate/unemployment rate, job take-up and losses;

- Manufacturing output and rate of growth;

- Economic growth in terms of GDP and other key statistics

Most of the focus on such factors is on domestic performance although, given how interconnected the global economy is, many investors also monitor such indicators on an international basis. The key objectives of any investor being to stay ahead of market trends of demand and supply, costs of borrowing and consumer sentiment!

How does this affect real estate, specifically multi-family?

Of the above indicators, consumer spending is probably the most important indicator for the real estate sector as, as consumer spending trends move, the real estate industry tends to move with it.

If consumer spending sentiment is negative or pessimistic, consumers tend to avoid making large purchases such as in real estate—but this may be good news for investors in the multi-family real estate sector. After all, a key upside of multi-family investing is the constant demand for rental accommodation in mature and developing markets.

Some things which may occur in the multi-family REPE sector in the event a recession, or at least a slowdown in the economy, appears imminent, include the following:

- demand for rental properties increases as consumers delay decisions to buy properties in view of affordability issues or expectations that they may be able to acquire at reduced prices later;

- existing investors can further optimise their acquisition and operational strategies to ensure controlled operating costs, achieve high lease-up rates and minimal vacancies;

- in view of rising interest rates, many multi-family investors may look to reduce their leverage or debt levels;

- if the FED sees a major slowdown on the horizon, it may defer or postpone increases in interest rates to be less frequent as planned, keeping the cost of borrowing at more affordable levels;

- investors may diversify and recession-proof their portfolios by selecting those markets and properties which show the optimal mix of economic drivers to support high occupancy — despite any impending downturn;

- some investors may move their investment capital to other real estate sectors thereby reducing competition for the better assets; or choose newer markets displaying population and income growth.

In short, investors in the multi-family sector have ways to mitigate the effects of any recession.

CPI Capital believes that yield curve inversion, whilst it cannot be ignored, is just one of a myriad of factors which affects the investment performance of real estate assets, especially multi-family properties.

We also believe that yield inversion is less a sign of the inevitability of recession, and more an indication of the possible timing of the next economic recession—yet there still may be underlying positive implications even if a recession occurs.

Lower leverage levels and different deal structures can be implemented, but some of our key strengths are our extensive experience and market knowledge and we are confident that we can continue to go forward with a two pronged strategy.

One is to remain as we are, with minor tweaks to our business plan, selectively acquiring quality property assets after exercising thorough due diligence on the market and subject property.

The other is to prepare ourselves for the further opportunities an economic downturn always presents.

Yours sincerely

August Biniaz

CSO, COO, Co-Founder CPI Capital

Ready to build true wealth for your family?

It all starts with passive income. Apply to join the CPI Capital Investor Club.

Search

Recommended