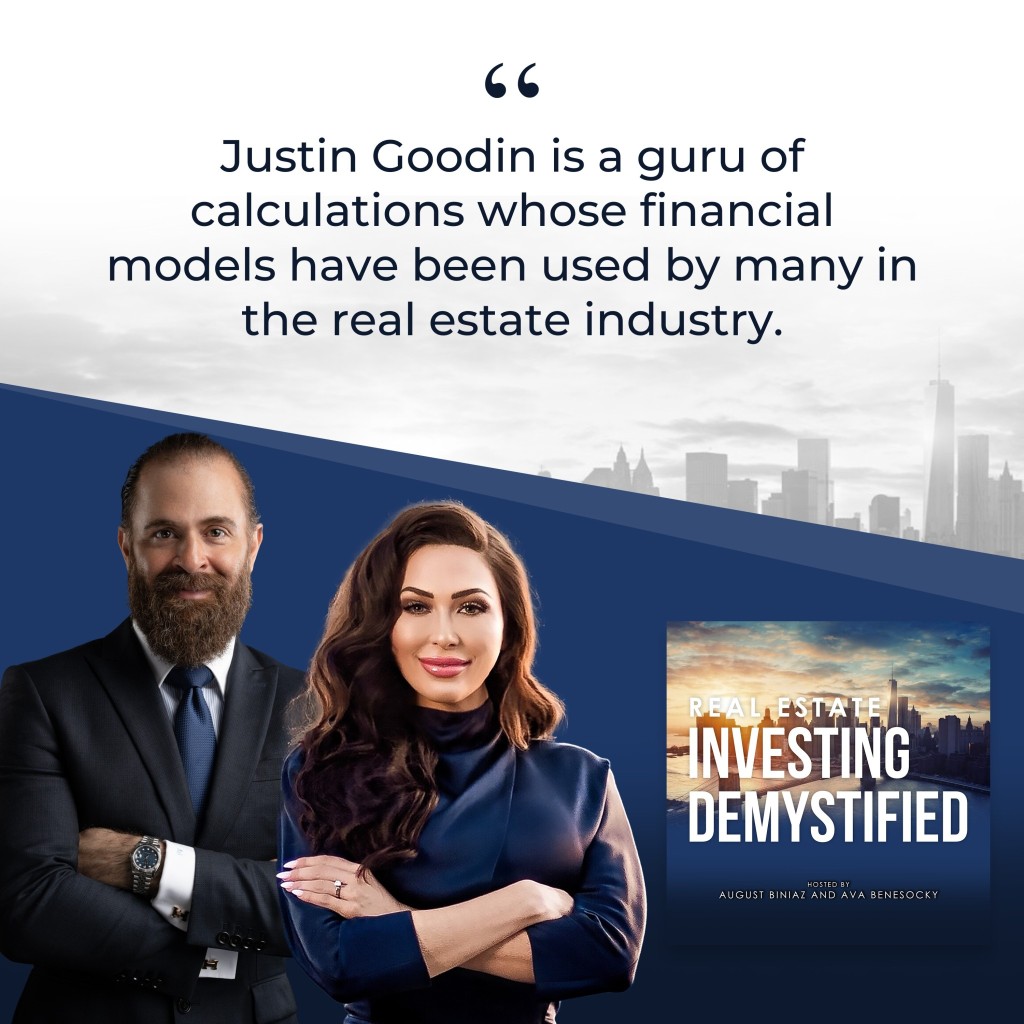

Are you ready to pivot from competitive value-add deals to sophisticated multifamily ground-up development? Ava Benesocky and August Biniaz welcome Justin Goodin, a former value-add partner who shifted his focus to building Class A market-rate and mixed-use multifamily projects in Indiana. He breaks down three important calculations on development, the importance of hiring of a construction manager, and his approach to structuring a $33 million syndicated deal. Justin also explains how he manages his time, keeps his pipeline full of new projects, and the various software his team uses for project and financial management.

Get in touch with Justin Goodin:

Website: https://www.GoodinDevelopment.com | https://justingoodin.com

LinkedIn: https://www.linkedin.com/in/justingoodin

YouTube: https://www.youtube.com/@JustinGoodin/videos

Instagram: https://www.instagram.com/justin.goodin

If you are interested in learning more about passively investing in multifamily and Build-to-Rent properties, click here to schedule a call with the CPI Capital Team or contact us at info@cpicapital.ca. If you like to Co-Syndicate and close on larger deals as a General Partner, click here. You can read more about CPI Capital at https://www.cpicapital.ca.

#avabenesocky #augustbiniaz #cpicapital

—

Watch the episode here

Listen to the podcast here

Important Links

- Justin Goodin on LinkedIn

- Justin Goodin on Facebook

- Justin Goodin on Instagram

- Justin Goodin on YouTube

- Goodin Development

- Goodin Development on Facebook

- Goodin Development on X

- Goodin Development on LinkedIn

About Justin Goodin

Justin Goodin is the founder and principal of Goodin Development, a multifamily development firm specializing in Class-A luxury communities throughout Indiana. Justin earned his bachelor’s degree in finance and supply chain management from Indiana University’s Kelley School of Business and spent several years as a multifamily underwriter for a local bank, where he developed expertise in commercial real estate finance and investment analysis.

Justin Goodin is the founder and principal of Goodin Development, a multifamily development firm specializing in Class-A luxury communities throughout Indiana. Justin earned his bachelor’s degree in finance and supply chain management from Indiana University’s Kelley School of Business and spent several years as a multifamily underwriter for a local bank, where he developed expertise in commercial real estate finance and investment analysis.

After gaining valuable experience in banking, Goodin transitioned to real estate investing, initially focusing on single-family properties before recognizing the benefits of large scale multifamily investments. This led him to establish Goodin Development and pivot toward market rate, mixed-use multifamily development projects. Based in Indianapolis, Goodin Development works closely with municipalities through public-private partnerships to create vibrant, high-quality housing solutions.

The company also provides busy families with opportunities to earn all the benefits that come with real estate investing, without the hassles of being a landlord. Notable projects include The Elwood, a $26 million mixed-use development in Kokomo featuring 114 Class-A residential units and commercial space, and District South, an 84-unit mixed-use project with office and retail components. Through these developments, Goodin has established his firm as a trusted partner for both municipalities and investors in Indiana’s multifamily market.

Multifamily Ground-Up Development With Justin Goodin – What Investors Must Know

Welcome back to the show.

We have a great show for you. We are actually super excited, Ava and I, because our guest is so experienced, so knowledgeable. I am going to be continuing to edify him on the preview of the show here. We are excited to learn from our guest. That is really the point of the show, to bring on expert guests for people to learn and enjoy it as well, and get entertained as well.

We have actually been following Justin for many years now. How many years do you think?

It has been at least five years.

On LinkedIn. We have seen him, but we have never actually met him in person, like face to face, like we are now. We have lots of questions and lots of fun topics to talk about.

That is the thing about LinkedIn. LinkedIn is a platform where different demographics hang out on different types of social media platforms. LinkedIn is particularly for business owners, a lot of people in business, finance, and particularly people in real estate who are thought leaders who are very well known. Spend a lot of time on LinkedIn. They quote LinkedIn a lot. They learn from LinkedIn. LinkedIn is the platform that they use. That is the feeling we have with Justin.

You feel like you know the person.

That is the whole purpose of it. Justin used to be a partner in a multifamily value-add firm. We saw a lot of information there. He is also a great analyst, and some of his financial models have been used by people whom I have known. He has added a lot of value to people using financial models. For people who do not know that, a simple Excel form is used to calculate performance for projects.

On larger deals like multifamily acquisition deals or development deals, these financial models get super complex. Our VP of Investments, Paul Hopkins, oversees that department, and one day I asked him, “I want to get a little bit more familiar with financial modeling, should I take some courses? How many hours do you think you have spent?” He almost smirked at me, saying he had spent thousands of hours on financial modeling, but AI these days is getting a lot easier. We are excited to have our show, looking forward to this.

Any points I missed here? We are going to give you guys a crash course on the world of development. All these structures that are getting built, housing is getting built for people. Housing is always great. Better places for people to live and more homes. It keeps prices in check as well. The more development that takes place, the more supply that comes online, which keeps those prices both for rents and purchase prices in check because supply is the biggest factor in prices.

August used to be in development. It is a very sophisticated world. You have been working on a project in Vancouver for many years. It is just about at its finish line. We know what it takes to develop a property. We are doing a build-to-rent deal right now in San Antonio, Texas. We know what goes on behind it. Let us welcome our guests to the show. Justin Goodin, thank you so much for being here with us.

Thank you so much for having me.

How Justin Got Into Multifamily Investing

Justin, let us just start things off. Are you still involved in multifamily? What is the current market and multifamily talk? Let us start off there before we get into development.

I am actively building and not existing multi-family projects. That is what you meant, but mainly just 100% focused on ground-up multi-family development here in Indiana.

That was not an opportunistic play where you focused more on the ground-up development of multi-family. Your company’s mandate is now solely on development, not acquisition of existing multi-family properties.

That is how I got my start, doing the value-add business strategy, which is still a very lucrative and fulfilling strategy, but I just made the pivot to go into class A market rates, multifamily, and mixed-use development here in Indiana. A few reasons for that. The biggest reason that comes to mind, and I am sure you guys know this as well, is that the value-added space is extremely competitive.

That whole space and niche has really blown up in the last 5, 10, 15 years. When that space blows up like that, it creates a lot of competition and causes a lot of the same companies to go after and chase the same assets, which drives down cap rates, drives up prices, and just makes that space very difficult to find deals that actually pencil out.

One of the biggest reasons I just felt this space was very inflated and very competitive. I spent over an entire year trying to find just one deal that penciled out, and I just could not do that. The prices just did not make sense of what sellers were wanting, what brokers were presenting prices for. I just spent a lot of trial and error and a lot of time just not finding deals. It just made it really difficult to continue buying and scale my business.

Not that development is not competitive on its own. It absolutely is. In the space that I am in, I am developing projects that are between 50, 100, and 150 units. There are not a lot of developers, at least here in Indiana, that are focusing on projects of that size. I found a really competitive edge going into that size project in Indiana. I am actually getting more deal flow, more volume, and doing more deals than I was on the value-add side.

The second biggest reason for making the pivot is, again, as you guys know, after buying the property and doing the asset management on some of these C-class and B-class deals and managing the contractors, managing the renovations, all the risk you are taking with going after and chasing that pro forma. A lot of risk and a lot of just unknown factors that go into the value-added space. A lot of people do not talk about it, but all that work and risk on the value-add side just made more sense for my goals and what I wanted to do long term to pivot into ground-up multi-family development.

I was going to say he mentioned that deals were not penciling out just really quickly on the same topic. As interest rates decline, there have not been a whole lot of deals that are penciling out. We can agree with you there. As interest rates trend downwards, where do you think the multifamily value-add market is going to be in that middle market space, 10 to 50 million?

Do you think there are going to be good multifamily value-add opportunities coming up here? Maybe we all thought that 2025 was going to present a lot of great opportunities. Distress is hitting commercial, trillions of dollars, and commercial real estate loans are coming to maturity. This is so exciting. We are going to get our hands on things. We found out that banks were like, “We are only really worth the value of the loans that we give out.

We want to make sure that these loans do not go belly up, and we want to try to work with the sellers so that they keep the property to continue managing it.” Kick the can down the road. Now it is 2026. Let us see what happens. We believe that 2027 is actually where opportunities are going to present themselves. Where do you think multifamily value opportunities are, if any are coming up here? What are your thoughts on what is happening in the next year or two?

It is still going to be a lucrative strategy. The value-added space is going to continue growing and thriving, of course. I do think a lot of older properties are going to be less competitive than they have been in the past 5 or 10 years or so. We are already seeing that. We are already seeing a lot of well-known buyers and institutions stay away from properties that are built in the ‘60s, ‘70s, and some even in the 80s. We are going to see a major pivot of buyers that are wanting the value-add space and opportunity, but not so much in the ‘60s and ‘70s asset.

Multifamily Ground-Up Development: Multifamily development will still be a lucrative strategy. The value of space will continue to grow and thrive, even though a lot of older properties will be less competitive.

Those assets are going to become very tough to sell in the coming years. There is going to be such a major shift of buyers still wanting to stay active, but they do not want all the deferred maintenance of the delinquency, all of the risk that comes with buying these older properties. People are going to continue buying these existing and value-add deals, but we are all going to see a major pivot into newer assets, 1985 and newer, 1990s and newer.

That old strategy of buying ‘80s value-add deals is, relatively speaking, that is like ‘90s today because that is what people have been saying since post-GFC, since 2011 and onwards. I just want to touch on the point you made, deals not penciling. People who are not experienced in this space every day and do not sit on a call with an acquisition team that I do twice a week to see what type of deals are coming to our pipeline.

Watching those deals coming in and either not trading at all or us writing a LOI and making it the best and final. The deal is just being traded to somebody else, not being acquired, because the price that the deal is being presented at is 20% or 30% more than what we are willing to pay for it. That all stems from what the LP economics are.

What is the investor economics we are trying to achieve for our investors? There are some levers we can pull. We can try to be aggressive and lower the GP economics to pump up the LP economics. We can be a bit more aggressive on our rent growth assumptions, on our exit cap. At some point, you are basically either fooling yourself or treading on the line of being unscrupulous when it comes to numbers, and then you factor in other fees that are associated with the GP as well.

If you are not achieving between 15% and 20% average annualized returns for your LPs, which is realized through cash flow the property produces, the yield, and then the upside on the back end, the deal is not going to make sense because most investors are going to go invest in different financial instruments that are going to be much less risky. We are going to touch on that in a moment as well.

Another factor is that people do not realize that commercial real estate is not like single-family. Single family, somebody passes away, there is death, divorce, other factors that people will sell no matter where the market is at. In commercial real estate, multi-family, and other asset classes, they will hold on. If they have to refi, they will hold on. There are some cases that they have to sell, but it is very far in between, and other groups come and gobble those up.

There are cases where deals just do not make sense, and people cannot buy deals. Groups that bought 30 or 40 deals a year have done two deals in 2025. That tells you where we are. In our group, we know that they did $5 billion of deals over the last ten years, and in 2025, they did not buy a single deal. Let us keep going here.

Transition From Multifamily To Development

Justin, we saw your post on LinkedIn about your $33 million development project that seems to be complete or almost complete. Was this your first development? A follow-up question to that would be, how did you go from being a multifamily value-add guy to literally being a developer? Again, we were touching on how sophisticated the development world is.

Going into development is definitely a whole other ball game within commercial real estate. It is not something that can just depend on your risk profile and how much money you have to spend and all the risk you can take with that, but if you want to get into development right and not make mistakes and be conservative. The way I did it was to get into my first project with a mentor of mine. This is a friend I have known for a long time, a good partner now as well. A mentor is how I broke into my first multifamily development deal.

Going into multifamily development is a whole other ball game compared to commercial real estate. It is not something dependent on your risk profile and how much money you have to spend. Share on XThat is the first one you mentioned. That is the $33 million project in Fishers, Indiana, which is just about ten minutes northeast of Indianapolis. This is a public-private partnership with the city of Fishers, 84 units, and about 20,000 square feet of office and commercial space. This was my first time breaking into the development space, partnering with someone who has already been in the space for about twenty years.

A lot of times, people, even myself, used to be a home builder for ten years. I knew everything about construction and what have you, but I did not understand development. My mom used to talk about Trump all the time. I am somewhat of a Trump supporter, but I have to be careful saying that these days, even though he is the president of the United States and is about to go to war any day now. He is probably going to hit Iran before the weekend here or sometime this week.

I used to see Trump’s name on these buildings, and people would right away assume that he was actually building the buildings. He is there, maybe swinging a hammer himself, and he is building these buildings. That was not the case. He did build the Trump Tower in New York. That was the project he did with his father in the ‘80s, I believe. In any other project he did, in any subsequent project he has done, he has not been a developer. He has not been a general contractor.

He has not been the investor. He has just lent his name and brand to the developer to build that project. That was his business strategy, to have people use Trump Tower the same way they use the Ritz Carlton or other big brands. The developer uses their brand to build these structures and so on. Taking that out of the equation, talking strictly about a developer, what is a developer?

Even people who are experienced like myself have this misconception that the developer is the general contractor, is the person who goes and actually hires the trades, hires the suppliers, oversees the project timeline, and deals with the city. A developer is not really that. A developer is really the mastermind behind a project, who somewhat oversees and brings in all of these professionals. Maybe touch on that a bit, if I am going down the right path here, Justin.

Thank you for bringing that up. It is a very key point that some people miss. To your point, a developer, I think of them as being like at the top of the pyramid, if you can picture that. A developer is leveraging their knowledge and expertise in the space. The developer has the vision of the entire project. They are going out and hiring all these different third-party companies to help them build the project. For us, we are not vertically integrated at the moment.

We go out, and we hire an architect, a civil engineer, and the construction company. We hire all these different companies to help us build the project instead of doing it all ourselves. You could ask me questions about the actual framing in the building or civil engineering questions. I do not know all these different aspects of civil engineering, architecture, or environmental engineering.

I go out and hire these experts to work with me on the project. I think of the developer as just having the vision, and they are putting the project together while leveraging the knowledge and expertise of other third-party companies to work with. To answer your question, our company is not building the actual project.

A multifamily developer possesses the vision to put a project together while leveraging the knowledge and expertise of third-party partners. Share on XWe go out and hire a construction management team that goes out there and hires different subcontractors to build it. They are managing the process for us. We are managing them along with reviewing the budget, reviewing costs, doing draw requests with the bank, and all the stuff on the back end to make sure the project goes smoothly.

Just to be the advocate of some development companies that are not vertically integrated, I would actually say in some cases it might be a better option because if you, and we have learned this with CPI here ourselves as well, when you are building the infrastructure internally and you are bringing on team members to do a certain task and duties and responsibilities, you are limited to that group that you have created.

Whereas, let us say a development company wants to bring in architecture internal, you are just limited to the architect you have in-house. Whereas if you want to go and use an external architect, you can go to all the firms out there and hire the best ones that you please. That is your only exposure to that firm and that service provider. Same thing for others as well.

GC, same thing. A lot of times, people bring in GC in-house, but there is a level of liability. It is fashionable, and it sounds sexy to say we are vertically integrated and do everything in-house. There are literally some advantages to having some of these service providers be external. At some point, it makes sense to do it internally, like a merchant home builder, like a D.R. Horton, obviously has the architect in-house. Some of these other groups bring their legal department in-house.

All of this creates a lot of different liabilities, and it makes sense sometimes and does not in other cases as well. A couple of other questions about these service providers I want to touch on are something I was very familiar with. I was somewhat familiar with it when I wanted to get into large-scale development, and transitioning from being a home builder was the concept of feasibility studies.

In the projects that you are doing, we talk about multifamily. You are not doing a build-to-sell project. It is not a condo project. At some point, you might sell the project, but it is a for-rent product. As you are chasing that yield that the rents produce. Have there been feasibility studies done? As the contractors you hired, the trades you hire, and the service providers you hired? Who does those studies to say, “Is your idea, the vision that you have, does it even make sense?” Is that something you guys look at, or have you got any experience with?

Really just me. I am really doing the whole cost analysis in the beginning, like all the underwriting, seeing that this project makes sense based on the rents, based on the market, and the cost. I am really doing all those things on the front end to see if the project makes sense. Our last three projects have been very similar in their own ways. They are unique in their own ways, but very similar.

In our last three projects, we have used the same construction company, the same architect, and the same civil engineer. Two of those products actually even used the same bank. We are taking what works on previous projects and using that again and again, and the same team members as well, just to save from making mistakes, trying to reinvent the wheel every time. Just trying to take away what works and bring that into each new project, and just be as consistent as possible.

Multifamily Ground-Up Development: We work with the same team on previous projects to save us from making mistakes or trying to reinvent the wheel every time.

That is an easy way to do it.

Genius because we have learned as well with some of our service providers. Now, our legal teams, our compliance teams, they are literally on our Slack channel dedicated to communications with them. It gets so comfortable and makes things so much smoother.

Justin’s Strategy For Development Projects

Justin, what is the business strategy for your development project? Is it to stabilize and then sell to an institution, or is it to stabilize, refinance, and then hold long-term?

I get this question a lot. I hate saying it depends, but it does depend on how the market is, how interest rates are, and what happens when we are going to lease it up, sell it, or hold it. To answer your question, we are looking to sell. We are looking to build the project, lease it up, and sell it as quickly as possible. The reason for that is that I want to focus on being a developer.

Back to your point, August, about when you are bringing in companies in-house, like construction or property management. I have a similar mindset around this topic because once you choose to lease the property and then hold onto it, you are now an asset manager, so now you have to worry about all the performance and communications with the property manager company.

It just adds one more thing to your plate. Similar thing. If you had an in-house construction company, now you are not just a developer. You are a construction company owner. Now you have payroll. Now you have more overhead. For our projects, for the time being, we are looking to just stay laser-focused on being a developer. That is building, leasing up, and selling as quickly as possible.

That way, I can take the win and move on to the next project. I enjoy being a developer. I enjoy looking for deals, underwriting deals, and the construction process. I do not enjoy asset management. I do not enjoy working with the private manager companies and dealing with the tenants and all that overhead each month. I am just looking to be a developer and continue doing more and more projects.

Market opportunistic.

Allow me to throw somewhat of a wrench into your vision here. When I was again going back to my stories of being a home builder, I was very inquisitive with these larger developers, and I would go for lunch with them at times. The guys who build the low-rise and high-rise, these huge projects. I was so excited to learn, and some of them actually did invest in value-add deals or at least existing assets.

My question was why bother? Why would you invest in this? Initially, they did not ask that. This was later on, pondering why they would do that. That was more about their balance sheet. They wanted to have a level of cash flow associated with their balance sheet to showcase when they went out, got loans, and that cash flow would keep them going in case something came up or there were calamities in their business.

A lot of developers get used to just rolling over because they really drink their own Kool-Aid, so they just roll over their winnings into the next deal. When the market goes bad, developers get hit harder than anybody else. They are not diversified because their next deal is the best deal possible, which gives the best returns possible. Diversifying into some, not necessarily value-added, but some cash-flowing deals is better, as that is what I have learned.

Breaking Down Three Calculations On Development

Let us get a bit complicated now, and you are the guru of calculations. When you do a development project for apartments, there is a calculation called yield on cost, another one called untrended yield on cost, and another one called unlevered yield on cost. Can you give us a quick description of what these calculations mean? Let us do that first before my next question. Can you give us a description of what those three mean? We will go to the next question.

Yield on cost is a really common commercial real estate metric altogether, but all kinds of different companies use this, no matter what asset class they are in. It is also important for the value-added space, but extremely important for development. Yield on cost is, the way I look at it, it is just like your yield of return after the property is leased up, stabilized, and cash flowing. Yield on cost. The calculation is your yield against your cost.

What that property is producing in income, as far as the NOI divided by your total project costs, or your all-in basis on the deal. That is what you spent on the deal to build it. You are looking at your return based on that cost. You take your stabilized yield or your NOI divided by your total project costs. That shows you what you are making on a return basis after the property is leased up and stabilized.

That is on an annual basis, obviously, right? You are talking about annual.

Correct. Untrended is just cutting out all the noise of rent growth. As real estate investors, we project a certain amount of organic rate increases or organic growth year by year. That throws in another variable in your underwriting, more guesswork, and it is more aggressive to some extent. Untrended yield on cost is just looking at the same calculation, but it cuts out the noise of rent growth.

Just looking at your top-line collected rents, minus your vacancy, minus your operating expenses, and then that stabilized NOI or net operating income with no rent growth associated with it, against your total project costs. That is your untrended yield on cost. Unlevered is just looking at returns on an all-cash basis. No debt involved. There are unlevered and levered returns. Unlevered is just returns on an all-cash basis, and levered returns, all the returns we look at after the loan or after the debt is involved.

Got a few questions for you there. When it comes to yield on cost, is it assuming that the property is only held for one year, or is it different types of yield on cost? You are analyzing a project that you are looking to build, stabilize, and sell. Are you just looking at the yield on cost that you are going to be making in your first year, or does it depend on your business plan? If your business plan is a three-year business plan, does it look at the average yield over those three years or the term of the project, or is it just for one year?

I look at yield on cost on a best-case scenario. I have my projected rents in my in-line model, and I calculate the rents as if the property was 100% leased up. Here is my top-line revenue number. I look at that. I add in my vacancy, my other income, and then I subtract out my operating expenses. I take my stabilized proforma, exactly what it is going to look like on a stabilized basis, and then calculate my NOI that way. Does that make sense?

It does. When somebody is looking at untrended yield on cost, they are assuming from the date the first shovel hits the ground, or even before that, that they are not factoring in any rent growth for that time period? I was getting confused, where I was thinking that the untrended yield on cost means that they are saying, “We are going to keep this property for five years after it is built and stabilized.

Over those five years, we are not going to put any rent growth.” Is it for that period, or is it in a period while it is going under construction that you are not adding any rent growth? You are assuming the rent growth of today. Which one is the untrended yield? This is getting super complicated, but people might be lost.

Strictly speaking, on the analysis part, looking at your underwriting model, not what is happening in real life after the project is built, you can calculate it that way. I am looking at it from an underwriting perspective. Untrended just has zero percent rent growth. Here are your projected rents. Here is your top-line revenue number if the property was 100% occupied.

You add in your other income, like trash, utilities, things like that, you are charging the tenants. Take out your vacancy, take out your expenses, and that is your stabilized NOI. Assuming you have those correct expenses, assuming you had those rents in real life, that is your projected yield on cost with no rent growth.

That makes a lot of sense. Last question that I have with this topic. You also mentioned, and Ava asked you about unlevered yield on cost. Why even have such a metric? Where does this even come up? Why do people even care?

I do not think unlevered yield on cost is too common in the space that I have seen. There are unlevered returns. You can look at returns on an unlevered basis, the IRR, equity multiple, etc. Some operators and some institutional groups like to see returns on an unlevered basis just to cut out the noise of debt and purely see what the returns are on an operational basis.

We all know that once you bring debt into the equation, into the deal, debt always enhances returns. I am not too concerned about the unlevered returns because I am always using debt for properties. Of course, most real estate investors are. I am always looking at returns on a levered basis or after debt becomes involved.

Justin, can you also discuss the difference between yield on cost and cap rate?

Human cause is looking at your yield in comparison to the total cost it took to build the deal. Cap rate is just looking at your return on your investment, more associated with existing multi-tenant properties. It is just looking at your NOI divided by your purchase price. Your cap rate might be six percent, which could be acceptable in some markets, but the cap rate does not have all your costs included in that deal.

You may have bought the property for X amount of purchase price, but how much did you spend on the property in your all in basis? How much do you spend on capex? The cap rate does not account for your capex or improvements you made to the property. The yield on cost does. It is taking your yield or your rate of return divided by your total all-in basis or your total project cost. Cap rate is just your rate of return on your purchase price.

Back Of The Napkin Underwriting Analysis For A Development Deal

Awesome for breaking that down for us. Next topic here, there is a way to underwrite a multifamily deal, and we call it the back-of-the-napkin underwriting or analysis. We will know quickly if the broker is out to lunch or not, or if the deal actually makes sense, and if we should even do a deeper dive into the underwriting.

That is really by seeing what the asking price is, what the current NOI is. What is a prevailing cap rate in the market where the rents are, if there is a value-add component, perhaps? Is there a back-of-the-napkin, quick underwriting analysis that you can do when you are looking at a development deal? Should you even bother with it or not?

Back to the yield on cost thing, I am usually doing a very quick back-of-the-envelope analysis for development and looking at that yield on cost and how it looks at the market cap rate. To answer your question, I am usually looking for a spread between my market cap rate and the yield on cost of about 1.5% to 2%. I want my stabilized yield on cost to be two percent higher than the cap rate.

On the back of the envelope approach, when I do my rough numbers about rents, costs, and my projections, I am solving for that yield on cost and spread number to see if it is higher than the market cap rate in the area. If it is low or negative, then I know something in the analysis has changed, whether that is cost, land, rents, or things like that. That is how I get a good feel, just for a quick look at development to see if it is feasible or needs some work.

I remember when Paul advertised to give out his back-of-the-napkin analysis at an event that he spoke at. Many people signed up for that. Let us go back to talking about your $33 million development project. I get really excited to talk about syndicating because I absolutely love raising money from investors, having the relationships. When a deal does pencil out, and they say, “Let us put this under contract and go ahead with it.” They really come to me and say, ” Ava, let us raise $10.5 million of equity” or “Let us raise $4 million of equity.” I absolutely love this part of the business.

You’ve got to see her cell phone with all the phone numbers that say accredited investors after the first name and last name. If she scrolls, it does not stop.

I have talked to about a thousand investors, accredited investors, over the last five years or so. I really enjoy that part of the business, but on your development project, did you syndicate that deal, Justin?

We are syndicating all of our development projects.

Do you want to get into syndication a little bit in August, or do you want to just focus on the development?

We have some questions coming up about syndication at some point.

Let us go into the next question. That is good to know.

LP Economics For Development Projects

When it comes to the profile, this is about the profile of the investors who get involved. At CPI, we are doing both development for sale products and similar to yours, more on the BTR side, and then multifamily value as well. The investor appetite and profile seem to change a bit. Obviously, investors who trust us and have done deals with us over the years and who have known us see us as their fiduciary.

They jump in on most deals that we have in front of them. Some investors who are somewhat newer are either a development-type investor or a value-add investor. That is really because of the yield that value-added deals produce. In most cases, value-add deals are cash flowing day one. These days, it might be a little bit harder, but historically, they have.

That gets advertised to investors that you are going to be making five percent cash flow over the average cash flow over the term of this project, this five-year term. They know that they have some cash flow coming. Psychologically, when you have some money coming in on an investment you made, at least you can sleep at night better knowing that there is some money coming in.

Development is not the case. Development is a situation where you are going all in. Obviously, there is the property, but there is no existing structure there, so it is not producing any income. You are waiting for all the upside on the back end. Overall, what type of economics are your investors? What LP economics are you trying to achieve on these development projects?

For our investors, you are correct. It is like a different appetite for development and a different risk profile. When you go into development, we work with investors who are not so much concerned or wanting to see a 5 or 6 coupon year over year. These are investors who have a longer-term mindset, and they understand the business plan, and they want more like an equity multiple at the end of the day.

They are not so much concerned with earning that cash flow. They want to see that big pop at the end, so they want to multiply their equity as fast as possible. As I mentioned, we are not looking to hold on to our properties for 4 or 5, 6 years plus. We are looking to build, lease up, and sell as fast as possible. That can help out the IRR when it is a faster sell. We are just looking to multiply our investors’ capital as quickly as possible at the end of the day.

Build properties as fast as possible so you can get a faster sale and multiply your investor's capital as quickly as you can. Share on XI was pleasantly surprised, actually, because we were doing multifamily value-add properties, and obviously, our investors were investing. When we presented our first development deal, the investor appetite was quite high. We did build trust with the investors, but they are like, “I would love to do a shorter term, two years.” I would love to have higher returns. I had cash flow for a couple of years. It was pleasantly surprising to see the investor appetite. I guess for you, you probably had a lot of multifamily investors that were on the multifamily value-add side that joined you when you launched your development deal as well, I am sure.

They had to have plenty of investors who switched over and trusted the process of development. There is one key distinction. We do start distributing cash when it is available. It is not just like the sale at the end of the whole period, but we do start distributing cash once the property is leased up and stabilized. There, it is just a normal syndication structure, just like that. Another key point is that investors are accruing that preferred return from day one. They are not earning that cash flow from the day of closing, but they are accruing that preferred return day one from closing as well. That helps align the sentence with investors, too.

Does the whole preferred return get accrued on an annual basis?

Correct. Date of closing, they are accruing that preferred return.

Time Management In Real Estate Development

Justin, this is a great question that I am looking forward to getting your feedback on. How is your time allocated managing a development firm that does all of this sophisticated stuff, like you were talking about? Also worrying about equity and debt. How do you manage everything? How do you allocate your time between all these sophisticated things that need to get done in a day?

I would say the majority of my time is keeping my pipeline full because, in development, I could find a deal or a pencil project tomorrow, and it could take a year before I even start that project. My biggest things I try to focus on are finding the next opportunity. On that first project that we did, the $33 million project, I had my next one breaking ground about six months before that one.

The first one is leasing up. Now on my second one, it is about 50% of the way through construction. I have my next one breaking ground this year. I am trying to keep my pipeline full because in development, it is similar to you guys, but you never know when your next deal is going to be your next opportunity. You always have to be continuing to look for new projects and look for the next opportunity.

That is the biggest thing that is going to move the needle in my business. I spend most of my time looking for new projects. The other bulk of my time is definitely on my current projects. Managing the job process, sending out wires to the contractors and vendors that we work with every month. That definitely takes a lot of time on its own. It is like a whole other job within development. Also, visiting the sites. I visit all my sites that are under construction on a weekly basis, manage the contractors, review the budgets, and just make sure things are staying on track and on time.

On the equity side of the business, when doing development, you can raise in tranches as well. You do not have to raise all the capital right at the front. It is not this big push to get all your capital up front. How do you approach it?

That is a very positive aspect of development because I could be working on a project for an entire year. I have time to notify my investors, answer questions, and give them plenty of notice before we actually need the funds. There is a lot of leeway in that timeline. Once we are between 3 and 4 months from breaking ground, then we are really pushing our investors to join us on the investment and help us fund the equity portion for it.

The rest of the equity after?

Correct. A key point, not all developers do this, but throughout that, whatever it is, eight months, a year that I am spending on the project to actually get it through the approval process and rezoning and working with the bank and city fees and all this stuff, I am putting all my capital upfront at risk and not raising capital from investors during that portion of time.

We are only getting investors involved once the property is fully rezoned, fully approved, and we are basically ready to start construction and close on the bank loan. That is only when we are getting investors involved, and we have a lot of capital upfront at risk for that entire year, and all the things we have to do to get that project shovel-ready.

For the land acquisition as well?

Correct.

Sometimes you can be creative and put a contract with the seller of the land that you do not complete until you have permits completing.

In terms of our contract, we usually try to give ourselves plenty of time. There have been times when we have had to buy the land before we actually had everything approved. We had a lot of confidence that everything was going to go through. We usually try to give ourselves plenty of time with the contract. We have to buy land first or do things like that before we are fully approved.

Software Used In Project Management And Budgeting

Justin, what kind of software does your team use for project management? What software do you use for budgeting? Obviously, to make sure there are no cost overruns. There is so much to keep track of. We know that prices change quickly. Let us talk about the software you use.

On the investment or investor management side, we are using Cashflow Portal. Really love Cashflow Portal for all of our investor software, sending out updates, distribution, and things like that. I also use that for my CRM and really AI for a lot of things as well. Nowadays, always use AI and ChatGPT to do several things in my business.

On the project management side, because obviously you oversee, even though the GC is autonomous, building the project, you have to oversee, making sure they are hitting the milestones on the project timeline and hitting the milestones when it comes to budgeting. Is there a software you use internally, or is it more just having Excel that supports you there?

For example, on a single-family home that August and I did together, we used Buildertrend. That was it.

That is more for single-family homes. A lot of builders use that because their clients can log in and see what stage the project is at. It does not work the best for larger development projects. These larger firms, those that do partner, that do have large development projects, they have an asset management team internally that is overseeing the GC, in most cases being external, and they have their own type of software.

Our partner, Paul, used to build bridges, and on these large bridge projects, they have dedicated people who are on the project management side, and they are using their own software, looking at the different parts of the bridge development projects. Is there particular software you guys use, or do you keep it high-level Excel, since the GC is doing all the actual day-to-day management of the progress?

Our construction company uses a software called Project Site, and then we basically just have an account with Project Site, and we are able to go in there and review budgets, check on timelines, and look at pictures every single day. Project Site is the software we use for development.

Plans To Expand The Team And The Business

It does both. It does budget and timelines. You talked about Indiana, Indianapolis. You are physically there, your project is there. Where were you originally from? Indiana?

Yes.

The reason you are there is that you understand the market well, you are from there, and your team is there. Any plans to expand, or do you feel comfortable? Every time I listen to experts talking about markets, Indiana always comes up as this sleeping giant. The slow and steady has done really well because it does not have the boom and bust cycles that these growth markets like the DFWs, Austins, Phoenix, and other markets have. Las Vegas and what have you. What is the market expansion that you are looking at? Is it to stay there or grow from there?

I love Indiana, born and raised here my whole life. My way of looking at that is I already live in just a fantastic market for not only living in, but investing in real estate as well. I do not have a lot of motivation to look elsewhere. I am already in a fantastic market with really strong fundamentals. I already started investing in real estate.

Not to say at a certain scale or down the road, 5, 10 years, whatever it may be, I might look in other markets or other states as well. For the time being, there is just so much opportunity here in Indiana. We do not have the boom or bust. It is very consistent, very steady for the last couple of years, while many of the nation’s largest cities were flat or even had negative rent growth in some cases. Indiana was still very steady at around 2% and 3%, while many cities were flat or negative. It is very consistent.

It does not have a lot of different fluctuations in the market. At the same time, I just like being within a few hours’ driving distance of our projects. Our construction company is great. They are fantastic. This is not a business plan where you can just hire the GC and say, “Just go build a project and let me know when it is done.”

You have to actively be walking around that site, reviewing your plans, and spotting things that are incorrect. Nobody else is going to catch that besides you, the developer, or maybe your architect, maybe somebody else, but there have been plenty of times where I have actually walked the site and found things that are incorrect mid-construction. You have to be hands-on. You have to be on the site actively managing these projects.

It is not something you can just hire and say, “Let me know when it is finished. I am sure everything will go well.” It is absolutely not like that. It is a lot easier for me to go do that and travel to these projects when they are under construction, if it is an hour or a couple of hours driving distance, versus getting on a plane and going across the country every time I have to tour a project under construction.

Since you are in this foundational part of your journey when it comes to development, it is a very important part as you are bringing on the right team members. You partner with somebody who is more experienced, and you are building that for yourself. When you are building your internal team members, who is the first person you want to bring on?

Is that somebody who has a GC type of guy who is going to oversee the external GC that you are going to be hiring? Is it a project management type of guy who understands project management? Is it a CPA who helps become a chief operating officer? Is it an investor relations guy? I am sure you have thought about this a lot, but as you grow, maybe you already have this person, but who do you feel is that first, integral, important person that is coming in? Who is that?

The first team member that I plan to bring on is a construction manager. Somebody who can do just what I mentioned, walking all of our sites every week, and somebody familiar with construction, who can spot incorrect things, who can go out there and catch things proactively when they are wrong per the plans.

Construction managers can spot incorrect things in a real estate development project. You can go out there while they check what is wrong on each site. Share on XWhen the time comes that I have multiple projects that are under construction at once, it is going to be really difficult for one person to drive to and walk all these different sites every single week. Bringing on a construction manager and somebody who can do that for me and who is familiar with construction, I think, would be a valuable asset to the team.

Current Status And Foreseeable Future Of Multifamily Development

A couple of more quick questions before we get to the next segment of the show. What is the long-term vision for Goodin Development? Is it right now an exciting space you are in, middle market, multifamily development in that market? Is that where you want to be for the foreseeable future?

Definitely for the foreseeable future. Yes, just staying laser-focused on what we are doing now. I am just building the same product, which is a class A market rate and mixed-use here in Indiana. Do not have any plans on building affordable properties, student housing, or lower-tier type assets. Really just focused on tha

Stay Sane in an Insane World: How to Control the Controllables and Thrive

t luxury A-class and market-rate type of property.

Last question before the next set of questions. We’re going to talk about this. It depends on our guests and their expertise. We switch this question around. Let us talk about the commercial real estate market, which encompasses multifamily development or multifamily value add, basically like that space. If the market cycle were a clock and the top of the market was 12:00 and the bottom of the market was 6:00, the top of the market would be mania.

There are non-refundable deposits, and people are just going absolutely berserk over deals. 80s, 90s deals are being traded at sub-four caps. The market is in mania. 6:00 is either in recession, or people are walking away from their deposits. The market is definitely in that recession phase. If you had to guess, what time is it today?

I would say 8:00. I would say we are coming out of some turbulent and bad times, but I do not think we are all the way out of those times yet. I am also still nervous about how AI is going to come into play in the next couple of years, like how that is going to do what it is to do for the unemployment rate, job growth, and tears. Some things are on my mind as well. I am very optimistic, especially in multifamily. We are coming out of the lower end of this cycle, but not in this expansionary period just yet.

Close to 6:00 or 8:00.

Justin, thank you so much for answering our question. We are going to get some more questions coming at you.

10 Championship Rounds To Financial Freedom

On the more personal side. The next segment of our show is called the ten championship rounds to financial freedom. I am going to ask you ten questions, and whatever comes to mind. Are you Ready?

Yes.

Let us go. Let us get into it. First question, who has been the most influential person in your life?

My parents. You want an explanation or just a quick?

Sure, it would be wonderful.

Parents have always been very supportive of me, my business, my goals, and what I have done in life. They have always been there for advice and suggestions, but have always been supportive in everything I do.

That is so sweet. Atlas and Apollo are one and two years old. Hopefully, they will be saying the same thing. I always love to hear that. That’s wonderful, Justin. The next question is, what is the number one book you would recommend?

Probably Stay Sane in an Insane World, written by Greg Harden. He was like the mindset coach for Tom Brady and other athletes out there, but it is more like a mindset book. Really recommend that book.

Let us add that one. August and I read for an hour together at night. Thank you for sharing. The next question is, if you had the opportunity to travel back in time, what advice would you give your younger self?

To start a business. I would go back in time to my teenage years and just tell myself to start a business. Not that there is anything wrong with working a W-2 or a career and climbing that corporate ladder. The more you are willing to take calculated risks, the more you are going to get those outside returns or oversight returns in your life. If you just go down the traditional, normal path, you are going to have a very traditional and normal life. Not saying you cannot have a great life with the W-2 and having a career, but starting a business can teach you so many different things and really be like that fast track to financial freedom for you.

Love that. Justin, next question. What is the best investment you have ever made?

The best investment ever made was a 16-unit property that I bought from a 30-year owner. This happened about three years ago. Found it from a cold email that I sent, bought it for super cheap, raised the value of it by doing a classical value add strategy, and sold it about eighteen months later, made like a hundred and eighty-nine thousand dollar profit in eighteen months. That was the best investment I have made so far.

Our developer guest’s best investment is a value add.

Justin, what is the worst investment you ever made, and what lessons did you learn from it?

I have not had any investments that have really gone wrong or gone that badly. I guess the worst one that comes to mind is my first investment, which was buying a single-family house on the west side of Indianapolis. This was a house. I really did not know anything about real estate, but I wanted to get into real estate. The first thing many people think of when they want to get into real estate is going, “I will go fix and flip a house,” or “I will go buy a rental.”

I bought a rental. I bought this shortly before COVID happened. It was a good investment before that. When COVID happened, and they had all the eviction restrictions, and you could not raise rents or evict everybody, this person stayed in the house for about a year and did not pay rent on purpose to abuse the system. I had to continue paying the mortgage by myself. He messed up the house when he left. I had to spend more money to fix up the house and ultimately end up selling it. It was not like a big home run in the end.

Sorry you had to go through that. Next question, Justin. How much did you need in the bank to retire today? What is your number?

Probably at least $5 million to retire.

It is a good number.

Using that to reinvest into cash-flowing assets and make more money along the way. I guess retire and do nothing, at least $5 million.

Next question. If you could have dinner with someone, dead or alive, who would it be?

I would probably say Elon Musk, just to hear his thoughts and thinking on different topics. He seems like a really interesting guy to talk with.

That is a good one.

Why not have lunch or dinner with the richest man in the world?

Justin, if you were not doing what you are doing today, what would you be doing now?

If I were not a developer?

Yes.

We have got to redo this question, but it is more about if you were younger, was there anything in sports you ever wanted to become? Was there anything in arts, music, or rock stars? Any hobbies you have on the side? Motorcycle riding? We had a guest who talked about being a hunter, and there would be a professional hunter. Anything there if it was not in the business and space you are in now, is anything you wanted to pursue at some point in your life that just did not work out?

I have been doing real estate for pretty much ever since I went down that entrepreneurship journey. I guess if I were not in real estate, I imagine I would have probably been working a W-2 or a career for a period of time and then starting some other form of business, whether that is a service-based business, a contracting business, I imagine. I would have my own business somehow.

A true entrepreneur.

It’s very structured.

My favorite question. Book smarts or street smarts?

Book smarts.

Two for today.

I have always just been more the person who does well in school, enjoys reading books, and it is more like on the educational part. I definitely think that I am more book smart than street smart.

Last question, Justin, if you had a million dollars in cash and you had to make one investment, what would it be?

I would buy some existing property to hold on to long term, whether that is a commercial real estate asset, such as multifamily, or some cash-flowing real estate asset, or I would buy a business.

I love it. Real estate investors are not going to like me very much. If I had a million dollars, I would buy Bitcoin at $67,000.

I would not do that.

Get In Touch With Justin

I know people are not going to like this very much. Justin, just let everybody know what the best way is for them to reach you.

Thanks for having me. You can find me on LinkedIn and Facebook just by typing my name, Justin Goodin. You can also go to GoodinDevelopment.com. On the front page, I have a free seven-day passive real estate investing 101 course. It shows you the ins and outs of passively investing in syndications right away. That is at GoodinDevelopment.com, and you can find it on the first page.

Thanks, Justin. It has been so nice getting to know you better. Putting a face-to-face.

It took a while. It took a few years, but we got you on.

That is awesome.

Thank you for coming on.

Thanks, Justin.

Thanks for having me.